By Adam Cmejla, CFP®

Sept. 7, 2022

Selling a practice that an owner has spent a good chunk of their professional life building should be both emotionally and financially rewarding. Among many other options, practice owners now have the option of selling to private equity (PE)-backed buyers.

The Lure of Private Equity

If you’ve followed anything on PE, then you know that it’s typical for PE-backed firms to offer a higher multiple of the selling practice’s EBIDTA (earnings before interest, depreciation, taxes, and amortization) than a private buyer. Whereas the typical cocktail-napkin valuation in an OD-to-OD transaction was ~65 percent of gross collected revenue, there are PE-backed deals exceeding 100 percent of gross collected revenue.

Is PE Really the Best Deal Financially?

Regardless of which way an owner decides to proceed, ensuring that you’re priming your practice for sale is always an important concept to focus on as part of being an owner.

In a $1 million+ practice, that’s not an insignificant difference, so it’s not surprising to have seen the volume of sales to private equity. However, how many owner/doctors have done a true deep dive into the math on selling to PE versus selling to an OD, taking the timeline of the sale and cash flow of each deal into consideration? The goal of this article is to do two things:

1. Acknowledge and clarify the contingencies that must be met when selling to PE, which will help us to…

2. Show the math on when it can actually be beneficial to sell to another OD at a lower valuation than what PE is offering…and by owning the practice for the years that they would be working post-sale for private equity, the owner comes out ahead!

Doing the Math on a Typical PE Sale Vs. Typical Sale to Another OD

Let’s set baselines and definitions for the example I’ll use to illustrate the two different transactions.

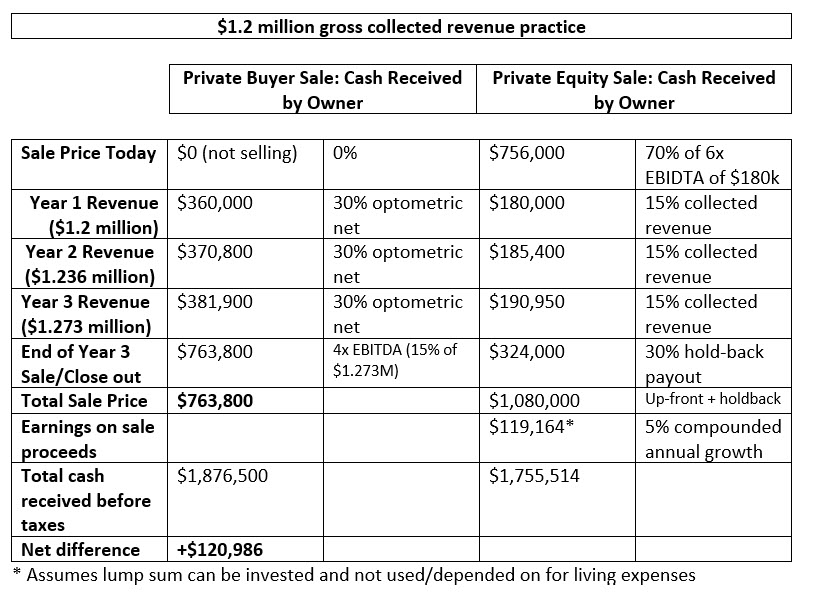

First, let’s assume this practice is a $1.2M gross collected revenue practice with a 30 percent EBOC (earnings before owner’s compensation; also called “optometric net”). This means that the owner is bringing home $360,000 per year in total earnings ($1.2M x 30%).

Let’s also assume that the replacement cost of the owner to provide optometric care equates out to about 15 percent of gross collected revenue, or $180,000. Remember that as an owner, you’re paid from your practice in two ways: the work you do IN your practice clinically and the work you do ON the practice as the owner. The former is what we define as your replacement cost: what would it cost for the business to hire an OD to replace the work that you do IN the practice clinically?

This means that the actual net operating income (NOI) to the practice owner in this situation is $180,000 or 15 percent of gross revenue ($1.2M x 15%). Note: there’s parody in this number as most PE deals will pay the (former) owner 15 percent of collections post-sale during the holding period.

We’ll assume that if the owner sells in an OD-to-OD sale (private owner sale), the practice will command a 4x multiple of their EBIDTA (earnings before interest, depreciation, taxes and amortization) while a PE sale would generate a 6x EBIDTA. Another note about the EBIDTA: for simplicity, we’ll assume that EBIDTA in this example is the same as NOI. The expenses of interest, taxes, depreciation and amortization can be different from practice to practice. Therefore, if we keep this constant the same in both examples the math will work out the same.

I’ll also add a nominal growth rate of 3 percent for each practice and assume the seller in the PE deal invests the initial proceeds from their sale into an investment account that will earn 5 percent compounded annually.

An important concept to understand when selling to PE: the valuation that is presented is never the amount that you’ll receive at closing. There will always be a hold-back that will be paid out either at the conclusion of your tenure at the practice post-sale or in a series of annual payments during your post-sale employment with your now-PE owned practice. Since this hold-back is not invested, and is essentially a zero-interest loan to the PE firm, the illustration below reflects the hold-back paid as a lump sum at the end of the post-sale deal. This is typically a three-year period. In this example, the PE sale will be a 70/30 up-front/hold-back split.

Important Considerations & Caveats

One of the most important considerations is whether you are physically, mentally and emotionally ready to continue working in “your” practice, which you no longer own. Selling one’s business will put an owner essentially through a grieving process, and each owner will grieve and experience that grief differently. Grieving involves the processing of emotions when we experience a loss. We typically associate grief with death, but a similar experience can be felt by owners on the backside of the sale of their practice.

While not everyone will experience the sale of their practice with the same emotions, it’s an important consideration to process how you feel about your practice because a sale to PE will almost definitely require you to stay on as a provider for three years post-sale. If you just don’t want to make this commitment, be honest with yourself and ensure that your financial plan can absorb the loss of cash flow from not working three years post-sale. If you’re not planning on working three years post-PE sale, you may decide to sell to an OD right away, thus giving up the future cash flow illustrated above during the three years that you’d still be the owner of your own practice.

Other Articles to Explore

Another important consideration is whether your lifestyle can absorb the decrease in income in a PE sale. As illustrated above, part of the total cash received in selling to PE is the investment return earned on the 70 percent lump sum that is paid out at closing. While no investment is guaranteed to earn any annualized rate of return, you are guaranteed NOT to make as much if your current lifestyle requires you to begin spending down the proceeds of your practice sale to supplement your cost of living.

Can you essentially live on half of what you were earning pre-sale, or will you be required to start spending down assets within your portfolio? If not, then prudent planning to determine what amount you can safely withdraw from your retirement nest egg in the most tax-efficient manner is paramount.

Lastly, the financial calculations above don’t take into consideration real estate that might be owned by the selling doctor. The benefit of selling to PE is that they will not be interested in purchasing the real estate, so it’s a “safe” investment for the owner to continue to hold. Most OD buyers will eventually want to purchase the real estate owned by the selling doctor, which can potentially disrupt a sale to another OD if the selling doctor wanted to keep their building.

In our experience, however, there are many options to ensure that all parties are taken care of with the real estate, including first rights of refusal on the property to protect the buyer, as well the opportunity for the seller to transfer equity from the sale of their building into another like property via a 1031 exchange, allowing them to defer any tax liability while also maintaining real estate exposure in their portfolio.

As you can see, there are a variety of considerations to evaluate when selling to private equity. It’s important to not let the big valuation dollars of a PE-backed deal mask the opportunity cost of selling. While it may be the best option for your plan, your personal plan and family deserve to know the full picture of all your options.

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNERTM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life. For a number of free resources, visit https://integratedpwm.com/ebooks/ and check out the “20/20 Money Podcast” to get more tips on making educated and informed financial and business decisions.

Adam Cmejla, CFP® is a CERTIFIED FINANCIAL PLANNERTM Practitioner and Founder of Integrated Planning & Wealth Management, LLC, an independent financial planning & investment management firm focused on working with optometrists to help them reach their full potential and achieve clarity and confidence in all aspects of life. For a number of free resources, visit https://integratedpwm.com/ebooks/ and check out the “20/20 Money Podcast” to get more tips on making educated and informed financial and business decisions.