By Robert Schultz and Jeanne Fletcher

Leasing can provide a cost-effective way to add instrumentation to your office. By fully understanding the terms of your lease, including penalties if you pay off the lease early, you can avoid surprises and save money.

When you are purchasing and financing equipment, have you ever wondered why you are steered into a lease? Would a loan be better for you? What is the difference? At Vision One, we have the option of providing loans or leases. We have chosen to offer loans because they represent, in most cases, a better deal for the ODs with more complete terms disclosure.

Loan Vs. Lease

Leases are generally more lucrative to the lender at a price to the OD. The differences are usually in the rates charged and the prepayment costs associated with leases. Many doctors use leasing companies in conjunction with purchasing new equipment and occasionally for remodel or relocation projects. You’ve probably used one yourself. It’s convenient and seems like a good deal. But, have you noticed there are no interests rates stated in the lease contract?

There is not a legal requirement to disclose a lease rate as there is for a loan. It is a complex task to calculate a lease rate because payments are made up front and there may be a final residual payment of up to 10 percent of the cost of the equipment. This obscures things, which allows most leasing companies to charge over market rates to ODs often times inclusive of rate premiums to cover referral fees.

Recommendation: Many leasing companies continue to charge up to 2 to 3 percent over market interest rates on equipment leases. To determine which rate is higher, compare the sum of payments on the lease (inclusive of any residual payment) to the sum of payments on a loan. If the sum of the lease payments is higher, then the lease rate is higher than the loan rate.

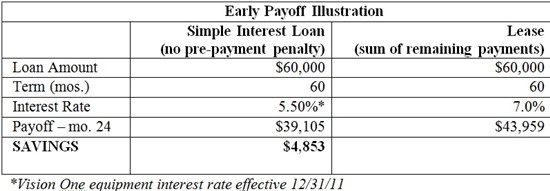

Beware of Pre-Payment Penalties

A majority of leasing companies will tell you that their leases do not have a pre-payment penalty or additional costs for early termination. However, the way the early payoff amount is calculated could mean that you owe more than the original loan itself! We know many of you prefer to pay off your loans or leases early so this could come as quite a disappointment.

Leasing companies have their own method for figuring your payoff when you want to terminate your lease. The most onerous case in the market, “sum of remaining payments,” is easy to calculate. Here’s what you do: Take your monthly payment, multiply it times the number of months left in the term, and that’s your payoff. The leasing company gets full payment, including all of the interest whether you pay off your lease early or not. That doesn’t sound like much of an incentive. Where’s your reward for paying off your lease early?

Most loans, including those from Vision One Credit Union, use a simple interest method of calculating your payoff amount that can save you thousands of dollars. Simple interest means you are charged interest on the loan balance for the time the loan is outstanding (be careful, some simple interest loans may contain a stated pre-payment penalty).

Recommendation: Before you sign your lease, have the leasing company provide a sample early payoff calculation. . .then you can decide.

Learn to Speak Lender-ese

As you have seen through these illustrations, lenders have a language all their own. You may believe the language means something it does not. Be sure to read and understand the contract terms before you sign to make sure there are no surprises. A good lender should always take the time necessary to explain the details of your loan or lease terms and answer all your questions before you commit. If you have questions or concerns about your lease or loan terms, you can call us and we will try and help you sort through it.

Related ROB Articles

Three Scenarios of Net Cash Flow: Is Your Practice Financially Healthy? Is it Salable?

Practice Budget Bootcamp: 3 Steps to Make Budgeting Easy

Robert Schultz is president and CEO of Vision One Credit Union in Sacramento, Calif. To reach him: BSchultz@visionone.org.

Jeanne Fletcher is executive vice president and chief credit officer of Vision One Credit Union. To reach her: Jeanne Fletcher @visionone.org.