Sponsored Content

By Bob Schultz

CEO, Vision One Credit Union

July 21, 2021

Many ODs, practice owners and first-time buyers are unfamiliar with the analysis required to determine practice cash flow adequacy. This can impact buying, selling and operating decisions. But what if cash flow adequacy can be simplified to one practice metric?

Vision One Credit Union is the only financial institution solely dedicated to independent optometric practices. It is all we do. Founded in 1951, by ODs for ODs, we are not for profit with an all OD, all volunteer Board.

Achieving optometric practice growth and value requires continuous investment and a long-term banking relationship. We take the time to know you, your goals and capabilities. Vision One Credit Union, because your team matters. You will appreciate the difference.

Our full banking services include:

Practice Transitions – Practice purchase, startup, partner buy in, exit strategy development (with affiliates) and execution.

Practice Growth – Purchase or startup additional location(s), relocation, remodel, equipment loans.

Wealth Building – Commercial real estate, location consolidation (rollups). A full range of deposit services including interest checking, financial planning (with affiliate).

Time Savings and Convenience – We offer full-scope financial services needed by an optometric practice. As the only banking organization asked to present Management CE at major optometric events, we know the business of optometry.

(800) 327-2628

Monday through Friday

7:30 a.m. to 4:30 p.m. (Pacific Time)

www.VisionOne.org

The metric is “Ownership Premium” and is defined as the amount an owner(s) can earn over and above a normal market salary working as an OD. Conceptually, this values the risk of ownership and separates it from an associate salary, which has its own market value. It is the one metric that can verify the practice is performing above, at, or below peer performance. Ownership Premium can determine if the practice has achieved full value, or upon sale, if a price adjustment is warranted.

The concept originated as a request from Pacific College of Optometry to develop a simplified method of teaching students to determine if a practice was right for them to purchase. The challenge was to find one number that could determine the financial health of a practice. Data on well-performing practices developed by Mark Wright, OD, FCOVD, and confirmed by us at Vision One Credit Union, was used as a baseline. A combination of metrics defined Ownership Premium, which was then applied to overall practice performance and cash flow adequacy.

For Existing Practices

Well-performing practices should earn an Ownership Premium of 15 percent or more of collected revenue, before factoring in debt payments. The Ownership Premium concept can be applied to the practice entity as a whole or individual practice locations. It can be used for all revenue sizes.

For Practice Acquisitions

The 15 percent Ownership Premium can be paid to the owner if no debt is used for an acquisition, or a portion of the premium can be used to make debt payments. Almost all practice purchases, whether for first timers or additional locations, are financed. Fully financed practice acquisitions include the sale price plus working capital. The debt payments should only be made from the Ownership Premium discussed above. Debt payments should not exceed 10 percent of practice revenue for financed practice acquisitions.

If Ownership Premium on the acquisition is 15 percent of revenue and debt payments are 10 percent of revenue, then the amount of Ownership Premium remaining that can be paid to an owner is 5 percent of revenue (15 percent minus 10 percent). With only 5 percent available to ownership, you can see why achieving an adequate pre-debt Ownership Premium is important. Much less and the cash return on investment could go negative requiring the buyer to use their own money to make debt payments for single-location owners, or it will diminish overall existing cash flow from a multiple-location practice.

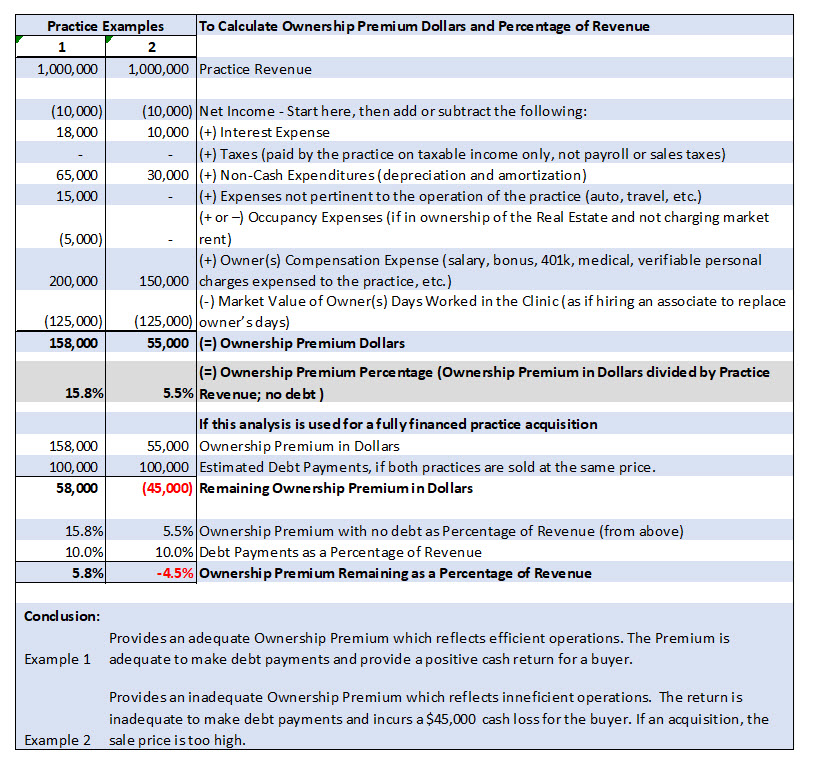

The chart below illustrates how to calculate the Ownership Premium in dollars. Divide the Ownership Premium in dollars by revenue to obtain the Ownership Premium Percentage. This calculation is a true version of EBITDA, which is used by practice buyers, sellers, many appraisers, and us at Vision One Credit Union.

Here are two practice examples, one with an Ownership Premium of 15.8 percent and the other at 5.5 percent. If both practices in the examples below are sold for the same price and are fully financed, the remaining Ownership Premium goes to 5.8 percent after the sale for the one practice example and the other goes to -4.5 percent.

Calculate your own Ownership Premium Percentage to see how you compare. If your number is 15 percent or better, great, keep up the good work. If it is below 15 percent, then you have some work to do.

For practices doing business with Vision One Credit Union, we routinely calculate Ownership Premium and other relevant metrics. It helps us determine if a practice can safely cover debt payments and provide a positive return for owners. As a complimentary service, upon request we will review our analysis results with our borrowing and depository customers.

Our mission at V1 is to enhance private practice optometry through innovative financial solutions. Our only market is independent optometric practices, since 1951. We constantly study industry problems. In most instances, we find workable solutions. If you are interested in this or other exit or growth strategies, you can contact me at BSchultz@VisionOne.org to discuss your needs.

Vision One Credit Union…Because Your Team Matters!

Bob Schultz is the CEO of Vision One Credit Union. To contact: BSchultz@visionone.org

Bob Schultz is the CEO of Vision One Credit Union. To contact: BSchultz@visionone.org