By Bob Schultz, President & CEO, Vision One Credit Union

SYNOPSIS

When seeking financing for a second practice acquisition, asking four key questions can help you toborrow well–and become profitable sooner.

FOUR KEY QUESTIONS ON FINANCING

WHAT AM I FINANCING? Borrow enough for the acquisition, working capital anda small amount for needed equipment and improvements.

WHAT IS THE TERM OF MY LOAN? Loan term is a more critical factor than interest rate in determining your total acquisition cost and overall debt management.

WHAT COLLATERAL IS REQUIRED FOR MY LOAN? Expect to pledge the assets of the practice you acquire and commonly the assets of your existing practice.

ARE THERE ANY HIDDEN LOAN TERMS? Insist on transparency in disclosure of interest rate, prepayment penalties and any additional loan terms or covenants.

“I was turned down for a practice acquisition loan, but I don’t know why.”

As bankers who specialize in lending to independent optometrists, we frequently hear that. The reason why: The OD had sought financing from a bank that doesn’t specialize in optometric practice acquisitions, and they likely dealt only with a business development officer not involved in the loan decision.

This underscores two primary mistakes that optometrists make in seeking financing. First, they don’t deal with a lender that understands them and the specialized needs of independent optometric practices. This would be like sending a person with eye problems to their primary care doctor for evaluation and treatment. Second, they fail to establish a personal working relationship with someone at the financial institution who can answer their questions directly, intelligently and add value to the process.

In order to facilitate communications and understanding, your financial institution contact person for this transaction should be a loan officer, involved with the decision making team and available to you from the initial loan application through funding. Your contact should keep you apprised of the status of the application throughout the process and be able to explain any issues and proposed resolutions that may arise. If done properly, your contact should be available for your subsequent practice borrowing needs and should help you understand the cash flow impact of your practice investment and financing decisions. To help you, at Vision One Credit Union we assign you a “Private Practice Banker” who knows you and your account.

Once you establish the right relationship with the right lending institution, you need to develop a “Project Budget” to identify the full amount of funds needed to purchase the practice and related items (see below). The process then breaks down to four essential questions you must ask and have answered to your satisfaction.

ACTION POINTS ON FINANCING

CHOOSE A LENDER WELL. Select a lender that specializes in financing optometric practice acquisitions and provides you a knowledgeable “Private Practice Banker” dedicated to your account.

UNDERSTAND LOAN TERMS FULLY. Do the math. Loan terms make a huge difference in the overall acquisition cost–and greatly affect your ability to generate satisfactory cash flow return and build up equity.

INSIST ON TRANSPARENCY. Head off unexpected or undisclosed costs and fees. Avoid vaguely defined terms of default.

PAY OFF THE LOAN EARLY. Paying off a 10-year loan in seven years saves you big money–and it frees you up to finance a needed office remodel or equipment update.

QUESTION #1:

What Am I Financing?

Acquisition price: When acquiring a 100 percent ownership interest in a practice, you should always buy “Practice Assets” and not stock of a corporation that owns the practice. Generally, an asset purchase excludes accounts receivable and cash, which remain with the seller. Asset purchases are standard in the industry and provide buyers many benefits such as limitation or termination of liability associated with the sellers practice (employment, divorce, vendors, etc.) and the ability to revalue the assets to market price and possibly take an IRS 179 deduction for a portion of the acquisition price (check with your accounting professional for advice).

Working capital: Working capital for a practice acquisition should generally equal two to three months of overhead. When you acquire a second practice, you must carry overhead until the cash starts to flow. The cash flow cycle = patient appointment, bill for services, collect billings. It could take a month or more to start to collect the billings. Unless there is a significant amount of private pay in the acquired practice, you can’t live on co-pays alone. You also need a base working capital level, which is the cash in the practice used to support seasonality of revenues, fluctuations of receivable collections, and making special purchases. At Vision One Credit Union, our Private Practice Bankers will help you establish a reasonable estimation of working capital which should be customized to the tendencies of the practice you are buying.

Needed equipment or improvements: Generally, there is not enough cash flow left over after the primary acquisition loan payments to support the additional debt and payments required to significantly improve the practice and provide a positive return to the buyer. If the practice cash flow can support some additional debt, it is best to include the improvements in the acquisition loan rather than to enter into a separate equipment loan or lease. Your Private Practice Banker at Vision One Credit Union can help you figure out how much debt the practice cash flow can support.

Sometimes practice buyers say they will just “lease” the equipment or certain improvements after the acquisition closes. Beware: Most leases have five-year terms and require higher payments, further diminishing remaining cash flow when compared to a 10-year loan.

In a lease situation, who is the customer? Have you ever felt pressured to use the vendor’s leasing company? Are you getting the best loan terms for your practice situation? Most lease companies obtain referral leads from the equipment and improvement vendors. In fact, most lease companies will pay the vendor a few percentage points for a closed loan. Loyalty develops between the lease companies and the vendors. To expedite the lease process, leasing companies rarely review the overall impact of the practice investment financing in context of practice cash flow and the owner’s salary requirements. As a result, we have seen many practices “over financed” with diminished cash flow due to the overzealous desire for vendors to sell and lenders to finance. Where is your Private Practice Banker in this

scenario?

Do not assume existing loans or leases: When purchasing a practice, you are buying assets from the seller free and clear of any debt. Occasionally, a buyer will be asked to assume an existing lease agreement as requested by the seller, generally so the seller can avoid hidden prepayment penalties (see below). This is a seller problem. If this is the only way the deal can move forward, the price of the practice must be lowered by the amount of the lease assumed. This can be complex, messy and may kill your loan approval as your primary lender now has to sort out collateral priority issues and effects of increased debt service as payments are generally much higher on assumed debt. Unsophisticated sellers may not be willing to reduce the price due to debt assumption, which is a deal killer.

QUESTION #2

What Is the Termof My Loan?

Loan term: This is the number of months / years over which the loan will be fully paid out. It is very important to get “term” right, even more important than interest rate. Never opt for a balloon payment which requires a large loan payoff after a portion of the payments are made.

Cash flow will be thin in a second practice purchase if you fully finance the acquisition and have to hire a fulltime OD to see patients because your availability is limited (see Acquiring a Second Practice: Six Tough Questions to Ask Yourself). Therefore it is imperative to pick a loan term that balances the various considerations: 1) practice net cash flow adequacy to pay debt service and provide a positive return to the owner; 2) total amount of interest paid (given the same interest rate, the longer the term, the more interest is paid); and 3) the timing of practice investment requirements that will necessitate additional financing (e.g., equipment, relocation, remodel, etc.).

Example: A practice to be acquired has gross collected revenue of $1 million. The practice sells for $670,000 and requires $90,000 working capital, therefore the loan amount is approximately $760,000. The seller is working five days per week seeing patients and an associate three days. The practice has net cash flow of 33 percent or $330,000 before the deduction of OD costs and capital expenditures (“CapEx”). $330,000 less $166,000 (OD costs) less $20,000 (CapEx) = $144,000 cash flow available for debt service and owner return.

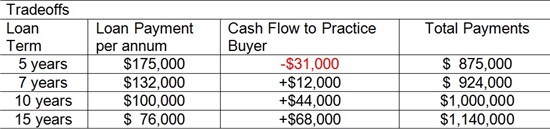

The followingtable shows how the term of the loancan dramatically affect the total amount that you pay in acquiring a practice.

As you can see in the table, there are a few tradeoffs to make when selecting a loan term. You can choose a short loan term of five years and payoff quickly and save on the total payments, but the cash flow is negative $31,000 per year. This can jeopardize your loan approval unless you can demonstrate the ability to comfortably carry the negative from your primary practice. The other extreme is to choose a 15-year loan term and generate $68,000 cash flow return per year, however your total payments (sum of loan payments) is $1.14 million on a $760,000 loan, which means the total interest charge is $380,000 ($1,140,000 – $760,000)! The Total Payments differences in the table are directly related to the additional amount of interest paid over the loan term. The longer the term, the more interest is paid. Who’s getting rich here, you or the bank?

How can I get the lowest total payments and still receive a positive cash return? At Vision One Credit Union we feel this can be accomplished by a 10-year loan term with a desire and opportunity to pay it off over seven years from the increase in cash flow you may generate from the practice over the loan term. This balances the need to have positive cash flow on the investment and minimizes the Total Payment Amount.

Additional Considerations: “Tips to Manage Debt Pressure”

1)The quicker you pay off the loan and payments terminate, your personal cash flow return will increase by the amount of the terminated payments.

2)It important to pay off debt as quickly as possible so you can build equity in the practice and prepare to remodel ($75,000–$200,000) within a reasonable time frame, generally seven years. Most practices borrow to remodel. You don’t want to add new remodel debt to existing acquisition debt.

3)Would you rather have:

a. The debt paid off at the end of year seven?

b. Or, in the case of a 15-year acquisition loan, have an outstanding balance of 64 percent of the original loan balance at the end of year seven? This equals $486,000 in the example of a $760,000 original loan amount. Now add $200,000 in remodel debt and you are up to $686,000 in overall debt. Feels like you are back to where you started!

Prepayment Terms and Penalties

Most institutions require prepayment penalties for paying the debt off early. At Vision One Credit Union, we have not used prepayment penalties. It is vital to make sure you can prepay the loan without penalty. This allows a borrower to accelerate loan payments, say, on a 10-year loan term and pay it off in seven years (as described above).

QUESTION #3

What Collateral is Required for My Loan?

Collateral is defined as the assets that will be pledged to the lender for security purposes as a second source of repayment. There are a few collateral combinations you might encounter:

1) Expect to pledge the assets of the practice you are acquiring (Practice 2).

2) Depending on the strength of your existing practice (Practice 1) or Practice 2 you are acquiring, you may be requested to pledge the assets of both practices.

3) If the existing Practice 1 and Practice 2 you are acquiring will be in separate corporations but have similar ownership, Practice 1 will probably be required to guarantee or become a co-maker of the loan to acquire Practice 2.

4) There should be no reason to pledge any assets as collateral from outside of the practice(s).

Pledging the assets of both practices will generally reduce or eliminate any down payment requirement that may exist.

QUESTION #4

Are There Any Hidden, Non-Transparent or Onerous Loan Terms?

Some of the most onerous terms relate to leases.

Generally there is no disclosure regarding interest rate. This has allowed most lease finance companies to build in a commission payment to the equipment or practice improvement vendor. We have seen commissions range as high as 3 percent. You, the lessee (borrower), are paying for this as it is built into the payments. A quick and easy way to determine how a lease compares to a loan is to sum the payments of both and compare. Remember, any residual payment, generally ranging up to 10 percent of the lease amount must be added to the sum of the lease payments. Loans generally payout completely over the term and many leases require a final payment of 10 percent of the total be paid at the end of the term. That is why you cannot just compare loan to lease payments. Leases generally have shorter terms and higher payments than practice acquisition loans and should not be used to finance any portion of a second practice acquisition (as described above).

Many lease contracts do not disclose prepayment penalties. When you call to get a payoff, you are usually quoted “the sum of the remaining payments” which includes the full interest charge as if the lease was paid off over the full term. This may be proper lease disclosure but you can imagine the surprise from practice sellers when they call for a payoff on leases that are a few years old and the payoff may be greater than the amount financed! Simple interest loans do not have this hidden penalty as you are only charged for the time the loan balance is outstanding.

The less knowledge a lender has of optometric practice finance, often times they will try and develop comfort by inserting additional loan terms. Most ODs don’t understand them. Generally these are found in the “Default” section of the loan documents or may be called “negative loan covenants” in the lending industry. One of my favorites we found was a “call provision” that stated “the loan may be declared in default if the borrower is out of compliance with lenders global cash flow requirement” which was not specified. Other terms may preclude any additional debt on the practice. Try to operate if you have a negative debt provision coupled with a prepayment penalty, 15-year financing and the need to renovate the practice in seven years. Where is your Private Practice Banker in this scenario!

Understanding how to properly financeyour acquisition and subsequent practice investments will save you time, money and surprises. The processstarts by developing a relationship with the right financial institution, one that understands your practice, communicates effectively, and treats you as a valued customer.

Related ROB Articles

Acquiring a Second Practice: Six Tough Questions to Ask Yourself

Getting There: Planning a Successful Optometric Career

Grow or Die: Complacency is a Practice-Killer

Bob Schultz is president and CEO of Vision One Credit Union in Sacramento, Calif. To reach him: BSchultz@visionone.org.