SPONSORED BY VISION SOURCE

By Thomas F. Steiner

Director of Market Research,

Review of Optometric Business

Vision Source is the leading alliance of independent ODs, with 2,700+ member practices and 5,500+ member doctors in the US and Canada. The organization is actively engaged in advancing the competitive position of independent ODs. Earlier this year, Vision Source commissioned the editors of Review of Optometric Business to develop an objective analysis of the current state of independent optometry and to identify strategic priorities for bolstering competitiveness.

>>>Click HERE for a COMPLIMENTARY download of the full report “Challenges and Opportunities in the Future of Independent Optometry<<<

This article distils one section of the full report, identifying how independents are currently positioned among the range of eyecare providers.

Conventional wisdom among business analysts is that small independent retailers will have difficulty surviving in a competitive environment dominated by mass merchandisers and online retailers. The logic supporting this assessment is that independents cannot match the prices, buying power, real estate locations or management sophistication of huge corporations. Nor can they compete against Internet providers selling the same products without the expense of a bricks-and-mortar office.

During the last century, small mom-and-pop businesses disappeared in many retail categories (grocers, druggists, clothing stores, bookstores, etc) — squeezed out by multi-unit retail corporations. There was a time when the same consolidation appeared to be unfolding in eyecare. During the 1970’s and 1980’s, retail optical chains rapidly increased their share of the primary eyecare market. They added thousands of new locations and introduced new dispensing concepts, such as one-hour eyewear, that attracted customers. But then the momentum slowed. Over the past 20 years, the market share growth of retail optical chains has flattened.

Much of the growth in optical chain sales over the past decade has been among mass merchandisers, primarily Wal*Mart and Costco. Since 2001, the mass merchandisers have grown from just over one-fifth of optical chain sales to nearly one-third. Big box retailers have become the chain optical format with the largest share of revenue. But during the second half of the last decade, mass merchandiser growth slowed, primarily because Wal*Mart reduced its openings of new optical locations. In 2011 mass merchandisers accounted for 9 percent of the primary eyecare market.

Currently it’s estimated that internet sellers account for 8 percent of all retail sales and 6 percent of vision correction device sales, including less than 3 percent of prescription eyewear and about 15 percent of contact lens sales. Inroads by internet sellers to date have not seriously undermined the financial health of independent ODs.

Facing-off against some of the most sophisticated retail corporations in the world, independent ODs, as a group, have not only survived, but many have prospered. Currently it is estimated that independent ODs (not affiliated with large eyecare corporations or ophthalmology practices) have a 53 percent market share of the primary eyecare patient population and a 42 percent share of primary eyecare revenue. Independent ODs’ share of revenue is lower than their share of patients because their capture rate of patients’ device purchases is much less than 100 percent. Ophthalmologists hold a 15 percent share of primary eyecare consumers. Corporate providers, primarily retail chains, control 32 percent of patients and 46 percent of primary eyecare revenue.

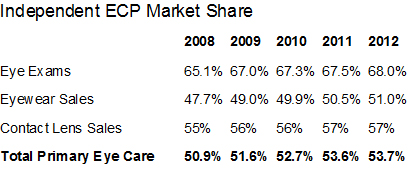

There is no ongoing national audit of the market share of independent ODs. But the Vision Council’s VisionWatch consumer survey measures the market share of all independent primary eyecare providers, most of whom are optometrists. Over the past five years, independents have enjoyed small gains in market share of both eyewear and contact lens sales and have maintained their share of eye exams. There is no evidence that the primary eyecare revenue of ophthalmologists has grown faster than that of independent ODs in this timeframe, so it’s highly likely that independent ODs have increased their market share.

Sources: Vision Council VisionWatch for eye exams, eyewear sales and total primary eye care; PAA estimates for contact lens sales, based on industry audits.

Sources: Vision Council VisionWatch for eye exams, eyewear sales and total primary eye care; PAA estimates for contact lens sales, based on industry audits.

The competitive position of independent ODs appears to be strong and sustainable, even given the clear challenges that they face. ODs have competitive strengths that the giant corporations are unlikely to undermine. By joining alliances with other independents, ODs are able to address many of their current competitive weaknesses.

The next article in the series will identify the major competitive strengths of independent ODs and suggest strategies to leverage these strengths.

Thomas F. Steiner, Director of Market Research for ROB, has spent more than 25 years helping eyecare practices succeed, including pioneering the introduction of color contact lenses into optometry. To contact him: tom.steiner@cibavision.com