First in a four-part series

By Mark Wright, OD, FCOVD

Review of Optometric Business Professional Editor

Nov. 29, 2017

What does the future of optometry look like over the next five years? The question was addressed at “The Future of Optometry,” a presentation at the 2017 Vision Expo West meeting that was sponsored by Essilor.

Mark Wright, OD, FCOVD, and Richard Edlow, OD, presented an analysis of a vast amount of information available from the U.S. Census Bureau, Bureau of Labor Statistics, National Eye Institute, Vision Council surveys, Centers for Medicare and Medicaid, Jobson Optical Group, Vision Watch, AOA Workforce Study, combined with original Jobson research. Panelists Gina Wesley, OD, and Michael Kling, OD, interpreted the data from the perspective of optometrists working daily in the trenches.

The presentation focused on four areas: demand, supply, mega-trends and opportunities. This article focuses on demand for eyecare services and eyewear.

Eyecare demand falls into two categories: demand for optical services and products, and demand for medical services and treatment, including surgery. The first category has been the traditional stronghold of optometry, and the latter has been the main focus of ophthalmology. That landscape is rapidly changing with medical services looming larger in the optometric profession in the years ahead.

Eyecare is a large business. More than three-quarters of the adult population wears vision correction devices. An estimated $33.5 billion is spent annually by American adults for refractive eye exams, eyewear and contact lenses, with an additional $28.6 billion spent for medical and surgical eyecare.

Demand for eyecare is higher among older people — both because a higher proportion of people over age 40 need vision correction and because the prevalence of chronic ocular diseases increases as people age. Growth in demand for eyecare has been steady and predictable, driven by population growth, the aging population, rising incomes and new technology.

The eyecare market weathers economic downturns better than most businesses because the foundation of eyecare demand is functional vision need, not discretionary desire. Simply put, people who can’t see need to see to function. Technical innovation is continuous and transformative in the eyecare market. New and improved corrective devices are constantly being introduced, and new diagnostic and treatment technologies steadily appear. Innovation is a significant contributor to demand growth, as it has been in other healthcare sectors.

As in all healthcare, insurers and government exert increasing influence on eyecare demand as the proportion of the population covered with vision insurance, medical insurance, Medicare and Medicaid expands. Third parties give eyecare practices access to patients. Doctors need to learn how to take patients beyond “just what the plan covers” in order to meet complete vision needs.

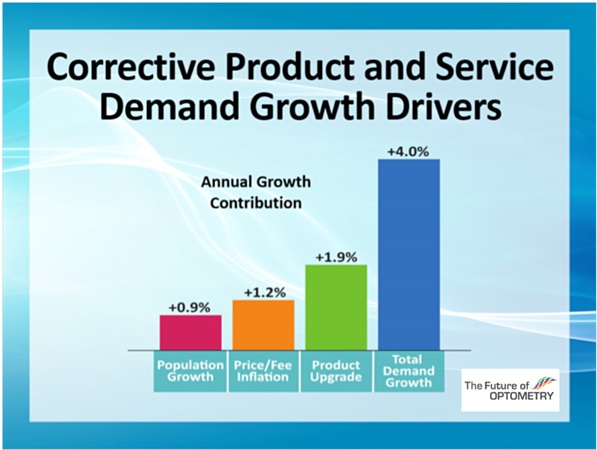

Over the past 10 years, the compounded annual revenue increase for optical corrective products and services has been about 4 percent in current dollars. While not spectacular growth, this rate of increase is nearly twice that of GDP growth and is one percentage point higher than compound annual growth of total consumer expenditures for all goods and services. The two most important eyecare demand drivers have been price/fee inflation and upgrading the product mix with new technology.

There is no reason to believe that the eyecare market growth rate will either accelerate or decline through 2025. Fundamental demographic shifts are improbable and the pace of technological innovation is likely to resemble recent history.

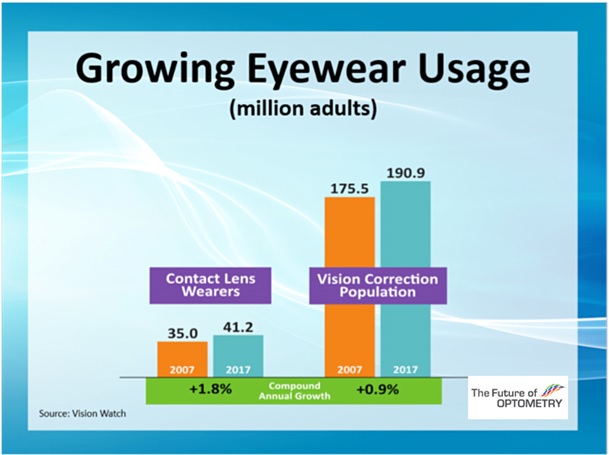

A long-term trend that has gradually changed the composition of demand for corrective products has been the increasing penetration of contact lenses. Since 1971, when soft lenses were introduced, there has been a steady rise in contact lens use. Over the past 10 years the contact lens wearer population has grown twice as fast as the vision correction population. Currently there are 41.2 million adult contact lens wearers, representing 22 percent of the vision correction population. By 2025, some 24 percent of the vision correction population are likely to wear contacts.

Contact lens growth has been driven by major new technologies including extended wear lenses, disposables, silicone hydrogel materials, and currently by daily disposable lenses. Going forward it is expected that contact lenses will continue to gain share of corrective product and service revenue, even as eyeglasses remain the dominant corrective device.

Most eyewear buyers are in the market infrequently – they visit an ECP only every other year or less frequently, even as most ECPs recommend annual visits. Independents can deliver better care and have tremendous revenue upside by reducing the interval between office visits. The “Think About Your Eyes” consumer campaign shows that the recall needle can be moved. Practices participating in the “Think About Your Eyes” campaign found the average patient return interval moved from 24 months to 14 months. This is significant.

Research shows the average eyeglass wearer uses just 1.5 pairs of glasses, and 63 percent of patients use but a single pair. These ratios have not changed appreciably in recent years, despite the rising affluence of the population and the proliferation of ophthalmic lenses and frame products designed for specialized uses or wearing occasions. The eyecare industry has been relatively unsuccessful in encouraging multiple-pair usage.

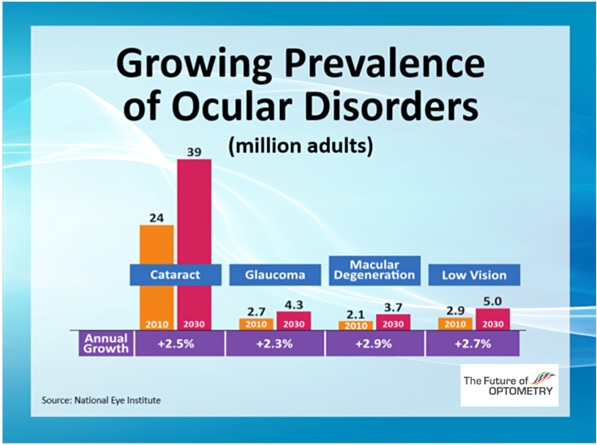

Among the fastest growing components of eyecare demand through 2025 will be medical eyecare. Medical eyecare services are expected to increase nearly three times as fast as comprehensive vision exams through 2025. The growth rates do not reflect fee increases, only the number of exams performed. The rapid growth in demand for medical eyecare relates to the aging population and to the growing diagnoses and treatment of prevalent ocular conditions such as dry eye and ocular allergies, as well as the expanded use of diagnostic tests such as retinal scans and OCT. According to the National Eye Institute, the number of Americans suffering from cataracts, glaucoma and macular degeneration will increase from 2.3 percent to 2.9 percent annually through 2030.

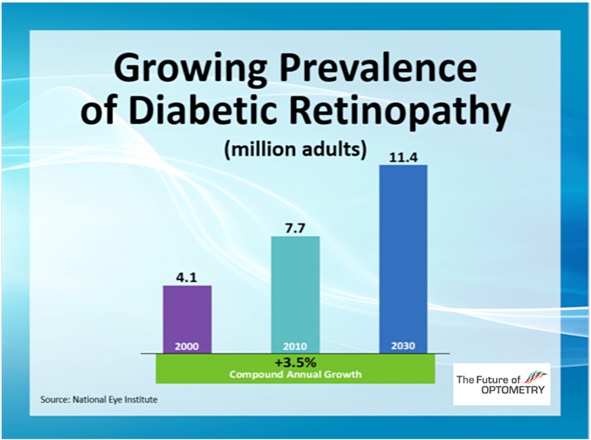

The number of diabetics is expected to also grow rapidly. Monitoring diabetic patients will become a major service provided by ODs, who with their large patient bases are well positioned to assist insurers to monitor this population annually.

Over many decades, managed care has become the largest revenue source for ECPs, now accounting for over 70 percent of total revenue in most independent optometry practices. This has happened as the Medicare and Medicaid populations have expanded and an increasing share of the population is covered by some form of medical or vision insurance.

One upside of the growth of managed care has been increased access to eyecare services for patients. A downside to this growth is that it is likely that some ECPs will not gain accreditation on provider panels and will lose access to a segment of their patient base.

Another downside is that consolidation in the insurance industry increases the leverage of the surviving insurance giants in dictating reimbursements, establishing administrative requirements and reporting standards. The uncompensated administrative workload shifted from insurance companies to providers continues to grow. With their enormous leverage over providers, managed care payers offer deflationary reimbursements that do not factor in rising staff, overhead and occupancy costs of doing business. This situation is unlikely to change in the years ahead. With the loss of control over fees, it will be increasingly necessary that independents increase office efficiency.

Over the next decade, the demand for both optical services and medical services will increase. This sets the stage for opportunities that would drive a positive future for optometry.

Action Plan to Capture Opportunities

1) Stay current with technical innovations in contact lenses, spectacle lenses, and disease management.

2) Create systems to take patients beyond “just what the plan covers” in order to meet complete vision needs.

3) Increase office efficiency in the area of patient flow.

4) Participate in “Think About Your Eyes” and list on the OD Locator.

5) Improve your recall systems. Identify why patients are not returning to the practice, and fix the problems found.

6) Create and manage systems in the office to promote multiple-pair sales.

7) Refine your in-office systems to manage patients with dry eye, ocular allergies, cataracts, glaucoma, diabetes, and macular degeneration.

8) Increase office efficiency in managing third-party patients.

Mark Wright, OD, FCOVD, is Professional Editor of Review of Optometric Business. Contact him: mwright@pathways-o.com.