By Bryan Rogoff, OD, MBA, CPHM

SYNOPSIS

Tracking your finances provides a guidepost for necessary changes. ABC Accounting practices give you another tool to do this effectively.

ACTION POINTS

ASSESS FINANCES, COMPETITIVE ADVANTAGE to invest more wisely.

GET OUTSIDE HELP if your practice is large and complex.

MAKE IT ROUTINE to conduct ABC Accounting to track financial progress.

When managing and tracking your practice’s finances, a structured process can be a great help. A tool that provides such a structured process is ABC Accounting. ABC accounting stands for Activity Based Costing Accounting, which is a subset of managerial accounting, which was my concentration when I received my MBA, and now is an integral tool I utilize to evaluate practices and businesses.

Editors Note: “The key difference between managerial and financial accounting is that managerial accounting information is aimed at helping managers within the organization make decisions. In contrast, financial accounting is aimed at providing information to parties outside the organization.” —Investopedia

The purpose of ABC Accounting is to improve the allocation of administrative and management costs and make better-informed decisions, especially regarding growth. Large corporations use ABC Accounting to improve their economies of scale, and it can be applied to smaller optometric and optical practices to develop short- and long-term strategies, and stay focused on activities that give your practice a competitive edge. For example, an optometric practice could utilize ABC Accounting to determine which frame lines, as well as personalized or custom lenses, are most profitable. Another example would be applying this accounting method to determine which instrumentation has been most profitable to the practice.

ABC Accounting assigns specific costs to specific activities, then to end products and services of your practice. This tool provides critical information about your practices’ resources and activities, and assigns a cost to perform them.

ASSESS FINANCES, COMPETITIVE ADVANTAGE

Why Bother with ABC Accounting? To Remain Competitive.

It is important for practitioners to understand ABC Accounting if they want to remain competitive in market. Companies sell your practice a new piece of equipment, inform you of the cost and/or lease agreement, let you know the average fee other practitioners are charging for the service or product (or reimbursement rates from managed care organizations), but it still may not be profitable. All practices are different and have different costs depending on geography, demographics, age of your practice, and resources. It should not be expected that profitability would transfer from one practice to another. ABC Accounting allows you to recognize how your personal practice costs relate to what is being sold (or attempting to be sold) to you.

ABCs of ABC Accounting: 5 Steps

Here are the basic steps of ABC Accounting general steps:

1. Make a chart outlining activities of the products and services your practice offers to patients from start to finish.

2. Classify each of those activities into two categories, value-added and non-value added. A value-added activity is something that increases the product’s service to your patient, not to your practice. And non-valued-added activities can be eliminated to reduce your practice costs without reducing your service and quality to the patient.

3. Once you have recognized the non-value-added activities, eliminate them.

4. Lastly, continue to evaluate your chart to improve efficiencies of the value-added services or replace them with more efficient ones.

Getting it Done: How to Do It, Step-by-Step

Make a chart outlining activities your practice provides to your patients. To keep things simple, let’s outline for chair time. Chair time varies from different types of examinations: comprehensive annual examination, contact lens, medical and follow-up examinations. We will evaluate the chair time based on 10-minute intervals, which will be allocated one unit.

Each practice is different and practitioners will have differences of opinion whether part of the activities will be value-added or non-value added, therefore it is important to get opinions from your patients and other colleagues to receive an objective perspective about how to refine your activities. Once this is done, a cost driver must be determined.

Again, since each practice operates differently, there is no formula to determine cost drivers. I would suggest starting off simple, and then refine your cost drivers once you become comfortable with the process. For chair time, this will be determined mostly from a fixed costs perspective, and not by variable costs. The different types of examinations will factor variable costs associated to them.

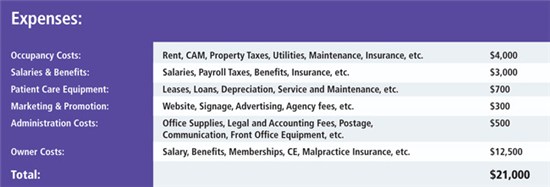

Cost drivers can be determined from your monthly profit and loss statement (P&L). Below is an example of expenses from a practice P&L that only handles examinations without a dispensary. Costs vary from all demographics and below are just arbitrary numbers. Make sure to include your salary and benefits as I placed under owner’s costs.

A cost driver is any factor which causes a change in the cost of an activity. A cost driver is the unit of an activity that causes the change in activity’s cost. Examples: In marketing, cost drivers are number of advertisements, number of sales personnel, etc. —Wikipedia

The monthly fixed costs for this practice is $21,000. This will vary considerably if you sub-lease space, own the property or lease in a free standing or retail space, as well as costs of utilities, labor, insurance, etc.

Your practice is opened five days per week from 9 am-6 pm, Monday-Friday, with one hour off for lunch. With this schedule, the total monthly units available is (based upon four week month): each unit is 10 minutes long: 6 units per hour x 8 hours per day x 5 days per week x 4 weeks per month = 960 units per month of chair time.

So your chair time cost is $21.88 per 10 minutes ($21,000 / 960) and your practice schedules comprehensive examination appointments every 15 minutes, which has a cost factor of $32.82 per appointment. There will be variable costs associated per examination that is being ignored for this example. Any fees collected above the cost factor, plus variable costs, is profit. Any appointment not booked, or is a no-show, is an opportunity cost which costs your practice $32.82 per appointment. Knowing your chair-time costs, and variations of how appointments are booked will allow you to adjust your schedule to maximize your examinations and lower your opportunity costs.

In microeconomic theory, the opportunity cost of a choice is the value of the best alternative forgone, in a situation in which a choice needs to be made between several mutually exclusive alternatives given limited resources.–Wikipedia

MAKE IT ROUTINE

Conduct ABC Accounting Process No More than Few Times Annually

The ABC Accounting process is typically is not performed as an everyday process, but can be done monthly, quarterly, biannually, etc., to improve productivity. Expect that there will be learning curves during the process while evaluating your activities and cost drivers. Analysts and consultants should always consider including feedback mechanisms and benchmarking goals to remind you to reevaluate. Expect to have a lot of adjustments in the beginning.

After Long Process, What Will I Learn?

The key metric is profitability of EACH activity and service your practice provides, which ultimately leads to overall profitability. Practitioners will learn how to improve efficiencies to eliminate non-value-added products and services, as well as understand how cost drivers are derived in order to improve productivity. Because they are arbitrarily tailored to your practice, they can be modified accordingly. This approach can improve stagnant growth, introduce and personalize new services and products, and provide different channels how to market, which financial accounting may not uncover.

ABC Accounting: Best Practices

Find a consultant who outlines a step-by-step evaluation process, strategies and feedback mechanisms to increase your ROI. On-site evaluation provides better insight to allocate cost drivers of your practice.

Remain objective regarding strategies to improve efficiencies, even clinical efficiencies.

Be collaborative, but learn how the process is done.

Understand that there are different formulas to increase profitability, not just decreasing costs, and increasing revenue, although that is a basic formula. Large corporations take into account marginal costs and other fixed costs that may not be apparent.

The results of any financial assessment should never decrease quality of your services and products. Benchmarking and other metrics should always be evaluated on a continual basis for improvement. Watch out for fads. No matter how good an idea is, sometimes it doesn’t always work. Each practice is unique and common sense can go a long way.

Related ROB Articles

Key Financial Metrics to Track–and Improve–for Profitability

Getting There: Planning a Successful Optometric Career

Practice By the Numbers: Track Your Key Expenses

Bryan Rogoff, OD, MBA, CPHM is an ophthalmic practice and healthcare consultant who operates from the DC/Baltimore market specializing in best operational, financial, and clinical practices. To contact him: bmrogoff@comcast.net

Editors Note: CPHM is Certified Professional in HealthcareManagement

The comprehensive CPHM program covers recent trends in the healthcare industry, and delivers valuable insights into:

-

U.S. healthcare systems

-

Health economics and strategies

-

Legal and ethical issues in healthcare management

-

National healthcare policies

-

Healthcare leadership and management

Those who become certified in CPHM must renew this credentialevery two years